Inflation exerts its influence across diverse industries, and the insurance sector is no exception. Although insurance is often viewed as a stable sector, companies within it can experience varying degrees of impact from inflation. Recognizing this, businesses must remain cognizant of how inflation affects the insurance industry and formulate strategic responses to navigate the evolving landscape.

In particular, insurance agencies are grappling with escalating costs attributed to factors such as rising interest rates. As per a report in the US, inflation has played an outsize role in the 5% to 7.5% increase in P&C claims payouts in 2022 across five key markets globally.

Fluctuations in mortgage rates and disruptions in the supply chain, among other significant market shifts, are contributing to the complexities faced by insurance agencies.

Though one may have limited control over the global economy, insurance enterprises can proactively establish policies and procedures to safeguard the company against the impacts of inflation. Specifically, making strategic investments in insurance technology can position the business securely to mitigate the effects of inflation. In this article, we explore several strategies to stay ahead of the challenges posed by inflation.

How Does Inflation Impact the Insurance Industry?

Inflation can diminish a business’s spending power, reducing its ability to invest in insurance technology. The declining purchasing power, coupled with increased costs of goods and services, may discourage businesses from making advancements in insurance technology. Let’s see how the inflation rate impacts the insurance industry-

-

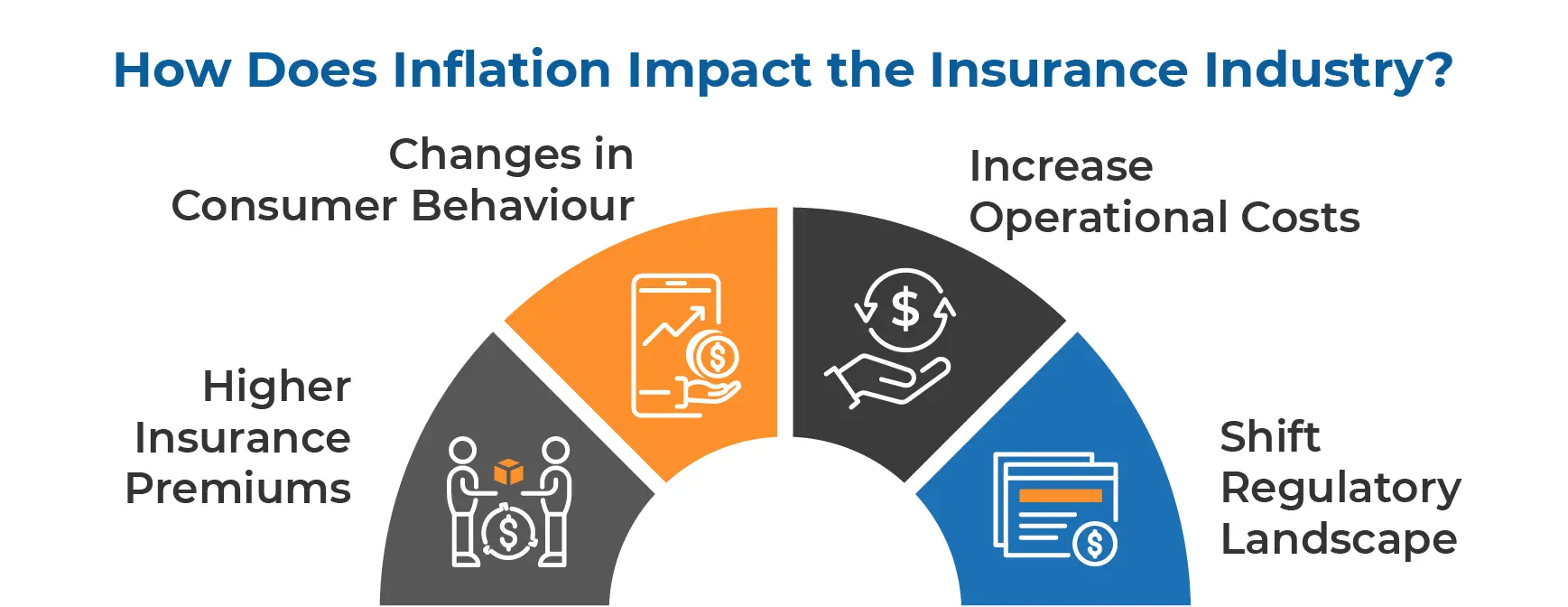

Higher Insurance Premiums

Inflation can make things more expensive, and this affects insurance in a few ways. First, when things cost more, insurance companies have to pay more for fixing or replacing damaged property and covering labor costs. This increase in costs leads to higher insurance claims, and as a result, insurance premiums go up.

According to a report, claims costs have risen by an annual average of 16% over the last five years. Additionally, when prices are rising a lot (high inflation), it can hurt insurance companies’ investment earnings. The money they make from investing premiums might not grow enough to cover the growing expenses, making it harder for them to keep prices low for policyholders. So, inflation can cause insurance costs to rise both because of more expensive claims and lower investment earnings.

-

Changes in Consumer Behaviour

Similar to its impact on businesses, inflation affects consumers in various ways. In general, policyholders have an increasing sensitivity to rising prices, posing a challenge in finding a delicate balance between ensuring customer satisfaction and maintaining the business’s profitability. What is essential is an insightful understanding of the customer’s mindset, allowing for the seamless fulfillment of their immediate needs without jeopardizing the overall viability of the business.

-

Increase Operational Costs

As the scale of various expenses increases, companies will encounter higher operational costs throughout the insurance value chain. This includes increased expenditures on recruiting and retaining talent, handling insurance processes like claims, underwriting, and acquiring and maintaining insurance systems and software infrastructure. In essence, every aspect is expected to experience a rise in cost.

-

Shift Regulatory Landscape

Inflation frequently prompts adjustments in government or regulatory policies, particularly within the BFSI sector. In turn, businesses find themselves rushing to adhere to these changes and must implement them swiftly, sometimes even within a short timeframe. The demanding pressures can also have a lasting impact on how insurance businesses navigate the challenges posed by inflation.

Automation and AI – A Safety Net in Difficult Times

So far we have discussed how Inflation presents a myriad of challenges for the insurance sector, impacting everything from increasing claims cost to reallocating resources such as funds. However, the dynamic landscape of insurance technology opens up opportunities to redefine business paradigms and become a key player in instilling resilience and adaptability to navigate through inflation. Want to explore how? Here’s how the insurance industry can step up using automation and AI:

-

Go for DIgital Claims

Automating the claims process can have several potential benefits that may indirectly contribute to addressing higher inflation rates. While it may not be a direct solution to inflation, improving efficiency and reducing costs through automation can have positive effects. Utilizing automation and AI solutions can bring an 80% TAT reduction in claims processing.

As insurers are facing rising customer expectations for a faster and more transparent claims process, automation and AI bots can help in offering the same. For example, using an AI bot, insurers can route claims automatically according to claim type, location, and other factors, reducing claim assignment time and effort.

In addition to providing real-time claims analysis, artificial intelligence can detect potential fraud and reduce claim leakage. By analyzing historical claims data, AI can also identify patterns and insights that can inform claims processing and better decision-making.

-

Make Decision Data Driven

Many insurance companies often rely on intuition for their business decisions. Although this method may be effective in typical situations, the impact of inflationary pressures can introduce bias. In such scenarios, consumers tend to become more price-sensitive, necessitating a thorough comprehension of market sentiments.

Here, investing in automation and AI technology facilitates the seamless collection and analysis, and utilization of extensive data, enabling companies to make more informed decisions. For example, insurers have data accumulated at multiple places; here, insurers can use AI to create a centralized data system that can be extracted using an intelligent document processing solution. With all data in one location, insurers can quickly get data insights and make data-driven decisions for claims, policy issuance and others.

-

Create Seamless Customer Communication

Creating a customer-centric approach in the insurance industry involves prioritizing interactions that customers directly experience. By tailoring these experiences, ensuring meaningful engagements, and delivering value early on in the insurance process, companies can win customer favor and cultivate a sense of satisfaction. Happy customers are more inclined to remain loyal, even during inflation.

For example, using an AI chatbot, insurer agents can handle service requests raised by customers and offer them instant responses. Also, integrating WhatsApp and MS Teams with AI Bot helps employees eliminate the need to navigate multiple applications. This offers flexibility and promotes collaboration among employees and customers to access information anytime.

-

Sharpen Risk Awareness

In times of financial challenges or witnessing others impacted by unforeseen events, individuals often become more vigilant, seeking ways to safeguard themselves from potential setbacks. These challenges create an opportunity for insurance companies to showcase their worth by effectively handling inflation risk and offering financial stability, thereby granting customers a sense of security and peace of mind.

Using AI technologies like machine learning models, insurers can detect fraudulent activity in real-time by analyzing the information. Also, having data insights in one place enables insurers to take proactive measures to mitigate these risks, such as conducting further investigations or implementing fraud prevention measures. Additionally, having an automated system in place enables insurers to maintain changing regulatory compliance standards as automation technology keeps learning with the changing environment and keeps the compliance and regulations updated.

Conclusion

In summary, let’s acknowledge that inflation is an inevitable force. Instead of dreading it, insurers should proactively concentrate on developing resilience strategies to minimize its impact on technology investments, operational costs, capital availability, and consumer behavior. By taking timely and proactive measures, insurance companies can not only reduce operational expenses but also enhance customer experiences, adopt data-driven decision-making, and more.

Imagine a scenario where insurance businesses actively embrace the advancements in insurance technologies. Picture a world where these forward-thinking companies are better equipped to navigate the intricacies arising from inflation. The flexibility, sustainability, and insulation from inflationary effects achieved through such initiatives would position them as global leaders in the insurance industry!

The post Battling Inflation in Insurance with Automation and AI appeared first on AutomationEdge.

This is a companion discussion topic for the original entry at https://automationedge.com/blogs/battling-inflation-in-insurance-with-automation/